A CFO’s Technical Guide to India’s Embedded-Tax Neutralisation Mechanism

A technical analysis for CFOs, Export Finance Heads, Tax Heads and International Trade Advisors — legal position updated to the notifications in force as of mid-2026.

Why this matter before we define anything

For a country running a persistent trade deficit and aspiring to move up the manufacturing value chain, exports are not merely a source of foreign exchange they are the mechanism through which domestic capacity, employment and technology absorption scale beyond the limits of the home market. India’s policy architecture reflects this, treating exports with deliberate fiscal favour and applying a principle trade economists have long accepted: taxes should not be exported. Goods that leave the country should carry the value added domestically, but not the domestic tax burden, because embedding that burden in the export price hands Indian goods a cost disadvantage in foreign markets.

Under GST, this principle finds its clearest expression in the treatment of exports as zero-rated supplies under Section 16 of the IGST Act, 2017. Zero-rating is not the same as exemption: an exempt supply blocks input tax credit, whereas a zero-rated supply preserves it. An exporter may therefore either export under a Letter of Undertaking without paying IGST and claim a refund of accumulated input tax credit, or export on payment of IGST and claim a refund of the tax paid, either route ensuring that GST does not stick to the exported product.

The difficulty is that GST is not the whole of the tax an exporter bears. Long before a product reaches the shipping bill, it accumulates a layer of levies the GST credit chain never touches: the VAT and excise on the diesel that powered the inbound truck and the captive generator, the electricity duty on plant power, the mandi tax or market fee on agricultural inputs, the stamp duty on transaction documents, and the embedded fuel taxes buried in every stage of inland transportation. None is creditable under GST or refunded through the IGST mechanism, and each quietly raises the floor price at which an Indian exporter can compete.

These are the embedded taxes, also called blocked, non-creditable or cascading taxes, and they are precisely the residue RoDTEP is designed to remove. Understanding RoDTEP correctly begins with understanding what it is not: it is not a subsidy, a GST refund, or a duty drawback, but a distinct remission mechanism aimed squarely at the taxes no other channel reaches.

The concept and economic rationale behind RoDTEP

RoDTEP rests on a settled international norm reflected in the WTO Agreement on Subsidies and Countervailing Measures (SCM Agreement): the remission or refund of indirect taxes and import charges actually borne by an exported product is not a prohibited subsidy, provided the remission does not exceed the tax actually incurred. This carve-out, found in footnote 1 read with Annexes I to III of the SCM Agreement, is the legal spine of the scheme. So long as RoDTEP genuinely rebates unrebated embedded taxes and does not over-remit, it remains on the permissible side of the line between remission and prohibited export subsidy.

The economic logic follows directly. Where an exporter’s cost base carries taxes that competitors in other jurisdictions do not bear because those jurisdictions rebate them, the Indian exporter is structurally disadvantaged on price. RoDTEP restores parity by returning the residual, non-creditable tax incidence to the exporter as a transferable duty credit, thereby lowering the effective tax content of the export.

Why MEIS had to go

RoDTEP’s predecessor, the Merchandise Exports from India Scheme (MEIS), operated on an entirely different and legally vulnerable premise. MEIS granted freely transferable scrips calculated as a percentage of FOB value, untethered from any measure of tax actually borne. It was, in substance, a reward for exporting rather than a remission of tax.

That design proved fatal. In India — Export Related Measures (WT/DS541), the United States challenged MEIS along with the EOU/EHTP/BTP schemes, the EPCG scheme, the SEZ scheme and the Duty-Free Imports for Exporters Scheme. The WTO panel report, circulated on 31 October 2019, found that India had graduated from the special and differential treatment available to developing countries under Article 27 of the SCM Agreement and could no longer shelter its export subsidies under that provision. Critically, the panel held that MEIS scrips were a direct transfer of funds contingent on export performance a prohibited export subsidy under Articles 3.1(a) and 3.2 — precisely because their design, structure and operation bore no relationship to remitting taxes actually incurred. The panel recommended the withdrawal of the MEIS benefit.

RoDTEP was India’s structural answer. Announced in September 2019 and operationalised for exports from 1 January 2021, it was deliberately architected as a remission mechanism — rate-based, tied conceptually to embedded tax incidence, and administered through the customs system rather than as a discretionary reward so as to fall within the footnote 1 safe harbour that MEIS had failed to reach.

The legal framework: how the pieces fit together

RoDTEP is unusual in that it is jointly administered by the Department of Commerce (through DGFT) on the policy side and the Department of Revenue (through CBIC) on the disbursement side. Its legal edifice is best understood as a stack, each layer resting on the one below.

The enabling statutory provision — Section 51B of the Customs Act, 1962. Inserted by the Finance Act, 2020, Section 51B is the foundation. It empowers the creation of an Electronic Duty Credit Ledger in the customs automated system and authorises the issue of duty credit to exporters, to be maintained in that ledger in electronic form. This is the provision that makes RoDTEP a customs instrument rather than a DGFT scrip in the MEIS mould, a deliberate architectural choice, because routing the benefit through duty credit usable against customs duty reinforces its character as a remission rather than a cash transfer.

Objective: Four instruments, Four different purposes

Perhaps the most common conceptual error at the finance-function level is to treat GST refund, input tax credit, duty drawback and RoDTEP as interchangeable “export benefits.” They are not. Each addresses a different layer of the tax stack, and confusing them leads directly to either under-claiming or the far more dangerous problem of double-claiming.

The organising principle is that RoDTEP is the residual mechanism; it picks up what GST and drawback structurally cannot reach. GST and ITC address the creditable GST chain. Drawback addresses customs and excise duty on inputs. RoDTEP addresses everything else that is embedded, uncreditable and unrebated. This residual character is why RoDTEP rebates “such duties and taxes as are otherwise not being refunded under any other mechanism,” in the language of the scheme guidelines.

Embedded taxes covered—with practical illustration

The taxes RoDTEP is designed to neutralise are those that fall outside the GST credit chain and outside drawback. In practice they include:

- VAT and excise duty on fuel — the diesel consumed by inbound and outbound goods transport and by captive power generation. Petroleum products remain outside GST, so this tax is non-creditable and cascades into cost.

- Electricity duty on power consumed in manufacturing.

- Mandi tax / market fees on agricultural produce used as inputs.

- Stamp duty on export-related documentation.

- Embedded central and state taxes on transportation, including toll and fuel-linked levies through the inland logistics chain.

- Other unrebated local levies at the state and municipal level.

Illustration. Consider a Ludhiana textile exporter shipping cotton garments. The yarn arrives by road; the diesel powering that truck carried VAT and excise that never entered any GST credit. The dyeing unit runs partly on captive diesel generation and partly on grid power bearing electricity duty. The finished goods travel to Mundra by road, again on taxed diesel. The export documentation attracted stamp duty. None of these levies is recoverable through the IGST refund or through drawback. They sit silently in the FOB cost, and it is exactly this residue that RoDTEP is intended to return, as a percentage of FOB value under Appendix 4R.

What RoDTEP does not cover

RoDTEP is bounded on all sides by the anti-overlap principle. It does not rebate:

- Any duty or tax already exempted, remitted or refunded under another mechanism – this the core exclusion. GST already addressed through ITC or refund cannot be claimed again under RoDTEP.

- Customs duties on inputs already covered by drawback or by a duty-exemption scheme such as Advance Authorisation.

- Duties or taxes on inputs used to manufacture products that are themselves ineligible under Appendix 4R.

- Any incidence for which the exporter has taken benefit under a scheme that already neutralises that specific tax.

The scheme guidelines state this plainly: the rebate shall not be available in respect of duties and taxes already exempted, remitted or credited. In other words, RoDTEP is expressly the non-duplicative residual layer.

Eligibility

RoDTEP eligibility is defined generously on the “who” and narrowly on the “what.”

Who can claim – Both manufacturer exporters and merchant exporters are eligible; there is no requirement that the claimant be the manufacturer of the goods. There is no minimum turnover threshold for eligibility (the ₹1 crore threshold discussed later relates only to the annual return compliance, not to eligibility). Notably, there is no condition requiring non-availment of GST input tax credit; an exporter may claim RoDTEP and take eligible ITC, because the two address different tax layers.

Scope of exporter categories – Originally confined to Domestic Tariff Area exporters, the scheme was extended by Notification 70/2023 (8 March 2024) to Advance Authorisation holders (except deemed exports), EOUs, and SEZ units, with those categories governed by the separate rate schedule in Appendix 4RE. For SEZ units, benefit is contingent on ICEGATE integration.

Core conditions. The duty credit is subject to:

- The goods being physically exported, with a valid shipping bill/bill of export and a Let Export Order under Section 51 of the Customs Act;

- A RoDTEP claim declaration made at the item level in the shipping bill in the customs automated system;

- Realisation of export sale proceeds within the period allowed by the RBI non-realisation triggers recovery; and

- The export product being listed in Appendix 4R (or 4RE, as applicable).

Ineligible goods and categories

The exclusions live in paragraph 4.55 of FTP 2023 and in the Table annexed to the CBIC notification. As a matter of scheme design, categories that already enjoy neutralisation of the relevant taxes are excluded to preserve WTO consistency and to avoid double benefit. Historically excluded categories have included exports subject to minimum export price or export duty, certain restricted/prohibited items, products manufactured in customs bonded warehouses under Section 65, certain deemed exports, and goods that have already availed specified benefits.

The exclusion list is not static. Notification 70/2023 deleted serial numbers (viii), (x), (xi) and (xii) of paragraph 4.55 with effect from 11 March 2024, thereby expanding coverage to categories previously excluded (the AA/EOU/SEZ extension). Because Appendix 4R and paragraph 4.55 are periodically amended within the budgetary discipline of paragraph 4.54, the operative rule for a CFO is procedural rather than substantive: verify the current eligibility of each 8-digit HS code against the live Appendix 4R/4RE on the DGFT portal before pricing or claiming a rate or eligibility position taken twelve months ago cannot be assumed to hold.

Rates and Appendix 4R

RoDTEP rates are product-specific, expressed at the 8-digit HS (tariff item) level, and take one of two forms: a percentage of FOB value, or a fixed amount per unit of the export product. Where a percentage rate applies, it is frequently subject to a per-unit value cap, an absolute ceiling on the rebate per unit, which functions to prevent over-remission on high-value goods and to keep aggregate outgo within budget.

The schedules are:

- Appendix 4R — The mainstream schedule for DTA exports.

- Appendix 4RE — The separate schedule for AA holders (except deemed exports), EOUs and SEZ units, generally at lower rates.

Rates are determined by the RoDTEP Committee on the basis of the assessed embedded tax incidence per sector and are calibrated to remain within the annual budgetary allocation mandated by paragraph 4.54 of FTP 2023. This budgetary tether is why rates can be revised, and occasionally cut, mid-cycle — as the February 2026 episode demonstrated.

How to identify the applicable rate in practice: classify the export product to the correct 8-digit ITC-HS code; locate that tariff line in the current Appendix 4R (or 4RE if exporting as an AA holder / EOU / SEZ unit) on the DGFT portal under Regulations > RoDTEP; read both the rate and any per-unit value cap; and confirm the code is not sitting in an ineligible category under paragraph 4.55. Misclassification is the single most consequential error, because it simultaneously affects the rate, the cap and eligibility.

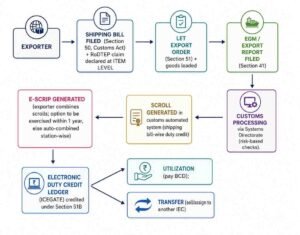

The end-to-end process flow:

Step-by-step:

- Declaration at filing. The exporter must make the RoDTEP claim by declaring it at the item level in the shipping bill in the customs automated system. This is a mandatory, one-time, at-source step – there is no facility to claim RoDTEP after the shipping bill has been processed without the declaration. This is the most common point of permanent loss.

- Let Export Order and EGM. Clearance and loading under Section 51, followed by filing of the export manifest/report under Section 41, are prerequisites to processing.

- Customs processing. The Systems Directorate processes the claim, including through risk-based selection criteria, in a manner analogous to drawback processing (Circular 23/2021).

- Scroll generation. Once processed, a scroll is generated in the customs system, containing the shipping bill details and the duty credit allowed against each.

- E-scrip generation. The exporter may combine duty credits across one or more scrolls at a customs station and generate an e-scrip in the electronic ledger. This option must be exercised within one year of scroll generation; if not, the credits are auto-combined station-wise and pushed to the ledger as an e-scrip.

- Credit in the ledger. The e-scrip sits in the Electronic Duty Credit Ledger maintained on ICEGATE, created for every IEC holder who either claims RoDTEP or receives credit by transfer.

- Utilisation or transfer. The credit may be used to pay basic customs duty on imports, or transferred to another IEC holder.

Electronic credit and the ledger

The RoDTEP benefit is entirely electronic. There is no physical scrip. Under Section 51B, the credit is issued as an e-scrip and maintained in the Electronic Duty Credit Ledger within the customs automated system on the ICEGATE platform. The ledger is created for each IEC holder, whether the original exporter or a transferee and is governed by the Electronic Duty Credit Ledger Regulations, 2021.

Credit becomes available for use only once it has crystallised into an e-scrip in the ledger, which in turn depends on the scroll having been generated (i.e., after customs processing) and the exporter having generated (or been auto-allocated) the e-scrip. From a treasury perspective, this means RoDTEP credit is not realisable at the moment of export; there is a processing lag between the shipping bill and a usable ledger balance, and this timing gap should be modelled in working-capital forecasts rather than assumed away.

The RoDTEP e-scrip: character, transferability and validity

The e-scrip is a transferable duty credit. Its defining legal features:

- Electronic only — held in the ledger; no paper instrument exists.

- Freely transferable — the credit, or the e-scrip, may be transferred to another person holding a valid IEC and registered on the customs system. This transferability is what gives the credit a secondary-market value: an exporter who imports little can monetise the credit by selling it to an importer who needs to pay BCD.

- Validity — The e-scrip carries a validity period from the date of its creation in the ledger (historically one year), within which it must be used or transferred; the transferee inherits the remaining validity.

- Conditional and defeasible — The credit is subject to realisation of export proceeds and to the cancellation/suspension powers of the customs authorities. If the underlying export is found non-compliant, the credit “shall be deemed never to have been allowed,” and recovery follows.

Utilisation: the single most restrictive feature

This is the point on which finance teams are most frequently, and most expensively, mistaken. Under the CBIC notification (76/2021 and 24/2023), RoDTEP duty credit may be used only for payment of the basic customs duty (BCD) leviable under the First Schedule to the Customs Tariff Act, 1975, on goods imported into India.

Can RoDTEP credit be used to pay… | Permitted? |

| Basic Customs Duty (First Schedule, CTA 1975) | Yes |

| IGST on imports | No |

| GST Compensation Cess | No |

| Social Welfare Surcharge / other cesses | No (restricted to BCD) |

| Anti-dumping / safeguard duty | No |

| Domestic GST liability | No |

The credit cannot be encashed by the exporter directly, and it cannot be applied against IGST, compensation cess or domestic tax liabilities. For an exporter with no import programme, the only way to realise economic value is to transfer (sell) the e-scrip to an importer. This narrow utilisation window is deliberate; it reinforces the scheme’s character as a customs remission rather than a cash subsidy, which is central to its WTO defensibility, but it has a direct commercial consequence: the realisable value of a RoDTEP credit to a non-importing exporter is the sale price of the scrip, which typically trades at a discount to face value.

The anti-double-benefit principle

If there is one doctrine that governs the entire scheme, it is this: the same tax incidence cannot be neutralised twice. RoDTEP rebates only the residual embedded tax that no other mechanism has already refunded, remitted or exempted. Where a duty or tax has already been addressed under another channel, that same incidence is off-limits for RoDTEP.

The interaction with each parallel scheme:

| Scheme | Interaction with RoDTEP |

| GST refund / IGST refund | Compatible. GST is a different (creditable) tax layer; refunding it does not bar RoDTEP on embedded non-GST taxes. Both may be availed. |

| Input Tax Credit | Compatible. No non-availment condition. ITC addresses GST; RoDTEP addresses embedded non-creditable taxes. |

| Duty Drawback | Coexists, but without overlap. Drawback addresses customs/excise duty on inputs; RoDTEP addresses residual embedded taxes. An exporter may claim both, but not for the same incidence. The “All Industry Rate” drawback schedule and RoDTEP are designed to be non-overlapping. |

| Advance Authorisation (AA) | Historically excluded; extended from 11 Mar 2024 under Appendix 4RE at reduced rates (except deemed exports), reflecting that AA already exempts duty on inputs. |

| EPCG | The scheme addresses capital goods duty, a different incidence; RoDTEP on the exported product is generally available, subject to the current Appendix 4R eligibility. |

| SEZ / EOU | Historically excluded; SEZ/EOU extended under Appendix 4RE (SEZ contingent on ICEGATE integration) at reduced rates, because these units already enjoy substantial duty-free input regimes. |

Compliance checklist

| Control point | Why it matters | |

| 1 | RoDTEP declaration made at item level in every shipping bill | Failure here is an irreversible forfeiture of the claim |

| 2 | Correct 8-digit HS classification of each export product | Drives rate, cap and eligibility simultaneously |

| 3 | Current Appendix 4R / 4RE rate and cap verified before each claim cycle | Rates and eligibility change mid-year within the budget |

| 4 | Confirmation the product is not in a para 4.55 ineligible category | Ineligible claims invite recovery |

| 5 | Scroll and e-scrip generated; e-scrip option exercised within 1 year | Lapse risks auto-allocation on unfavourable terms/timing |

| 6 | Export proceeds realised within RBI-permitted period | Non-realisation triggers recovery of credit |

| 7 | Annual RoDTEP Return (Appendix 4RR) filed if claims exceed ₹1 crore | Non-filing = denial of benefit + scroll suspension |

| 8 | Records substantiating embedded tax incidence retained for 5 years | Required for ARR scrutiny and RoDTEP Committee review |

| 9 | No double benefit on any single tax incidence across schemes | Core WTO and legal compliance condition |

| 10 | Ledger balances monitored for validity expiry | Unused credit lapses |

Worked example: the full lifecycle

Facts. Exemplar Textiles Pvt Ltd, a DTA manufacturer exporter, ships a consignment of cotton garments with an FOB value of ₹1,00,00,000. Assume the applicable Appendix 4R rate for the relevant 8-digit tariff line is 1.4% with no binding per-unit cap (illustrative rate — the actual rate must be read from the live Appendix).

Tax layers on the consignment:

- GST: Exported under LUT without payment of IGST; accumulated ITC of ₹6,00,000 claimed as refund under Section 16, IGST Act. → Addressed by GST refund.

- Input customs/excise duty: Drawback claimed at the applicable All Industry Rate on dutiable inputs. → Addressed by drawback.

- Embedded residual taxes: VAT/excise on diesel for inbound and outbound transport and captive generation; electricity duty on plant power; stamp duty on documentation. → Not addressed by GST or drawback, this is RoDTEP’s territory.

RoDTEP computation and flow:

- RoDTEP claim declared at item level on the shipping bill; Let Export Order obtained under Section 51; EGM filed under Section 41.

- Customs processes the claim. Duty credit ≈ 1.4% × ₹1,00,00,000 = ₹1,40,000.

- A scroll is generated for the shipping bill showing ₹1,40,000.

- Exemplar combines scrolls and generates an e-scrip of ₹1,40,000 in its Electronic Duty Credit Ledger on ICEGATE.

- Utilisation: Exemplar imports dyeing chemicals and applies the ₹1,40,000 e-scrip against the BCD payable on that import, a direct cash saving on import duty. Alternatively, having no import programme, it transfers the e-scrip to an importer, realising, say, ₹1,33,000 (a ~5% market discount) in cash.

- Proceeds: export sale proceeds are realised within the RBI-permitted period, so the credit is not subject to recovery.

- Annual return: if Exemplar’s aggregate RoDTEP for the year exceeds ₹1 crore, it files Appendix 4RR by 31 March of the following year, substantiating the embedded tax incidence.

The example crystallises the architecture: three different mechanisms (GST refund, drawback, RoDTEP) address three different tax layers without overlap, and RoDTEP’s value is realised either as a BCD saving or as scrip sale proceeds, never as a direct cash refund to the exporter and never against IGST or domestic tax.

Frequently Asked Question ( FAQ )

Can we claim RoDTEP and GST refund/ITC on the same export?

Yes. They address different tax layers —GST/ITC is the creditable GST chain; RoDTEP is the residual non-creditable embedded tax. There is no non-availment condition. The only bar is claiming the same tax incidence twice.

We are a merchant exporter, not a manufacturer. Are we eligible?

Yes. Both manufacturer and merchant exporters are eligible; there is no requirement to be the manufacturer and no minimum turnover threshold for eligibility. Note that if your annual RoDTEP exceeds ₹1 crore, ARR filing requires you to tie up with the manufacturer for input-tax data.

What is the single most common way exporters permanently lose the benefit?

Failing to declare the RoDTEP claim at item level in the shipping bill at filing. There is no retrospective claim facility. This is an irreversible forfeiture build it into your CHA/ICEGATE filing controls.

How long is the e-scrip valid, and can validity be extended?

Two years from creation in the ledger (extended from one year by CBIC Circular 21/2022-Customs). Unused credit lapses on expiry; a transferee inherits only the remaining validity. Monitor ledger balances for expiry.

Our company imports nothing. How do we monetise the credit?

The credit is usable only against Basic Customs Duty on imports. A non-importing exporter realises value by transferring (selling) the e-scrip whole to another IEC holder, typically at a discount to face value. It cannot be encashed directly or set against IGST/domestic GST.

What exactly can RoDTEP credit NOT be used for?

It cannot pay IGST on imports, GST compensation cess, Social Welfare Surcharge or other cesses, anti-dumping/safeguard duty, or any domestic GST liability. BCD only.

When must we file the Annual RoDTEP Return, and what happens if we don't?

If aggregate RoDTEP exceeds ₹1 crore in a financial year (across all 8-digit codes), file Appendix 4RR by 31 March of the following year (subject to any DGFT grace period). Non-filing denies the benefit and suspends further scroll-out until filed; a composition fee applies for late filing. Retain substantiating records for five years.

Is there a per-tariff-item nuance within the ₹1 crore rule?

Yes. If total RoDTEP exceeds ₹1 crore but no single 8-digit code exceeds ₹50 lakh, one ARR (for the highest-claim code) suffices. Where any code exceeds ₹50 lakh, a separate ARR is required for each such code, and separate returns apply for DTA vs AA/EOU/SEZ exports.

What happens if export proceeds are not realised in time?

The credit is deemed ineligible for the unrealised value. The RoDTEP amount, with interest under Section 28AA, must be repaid within 15 days of expiry of the FEMA/RBI-permitted period. Recovery provisions can also reach a transferee of the scrip.